Comprehensive weather insights help safeguard your operations and drive confident decisions to make everyday mining operations as safe and efficient as possible.

Comprehensive weather insights help safeguard your operations and drive confident decisions to make everyday mining operations as safe and efficient as possible. Learn how to optimize operations with credible weather and environmental intelligence. From aviation safety to environmental compliance, our comprehensive suite of solutions delivers real-time insights, advanced forecasting, and precise monitoring capabilities.

Learn how to optimize operations with credible weather and environmental intelligence. From aviation safety to environmental compliance, our comprehensive suite of solutions delivers real-time insights, advanced forecasting, and precise monitoring capabilities. Commodity Markets Curb Their Enthusiasm as U.S. Dollar Pushes Higher

In the first week of December, I concluded my analysis with this word of cautious optimism:

“The macro risk-on trade and optimism for economic growth outside of the United States is leading investors to pile into emerging markets and flee the U.S. dollar, further supporting oil and commodity futures more broadly…. Although with the coming vaccines we have a real reason to be optimistic for spring and summer 2021 crude and product demand, the December through March period remains perilous for physical markets…. Over the next few months, physical crude and product markets will be increasingly important to watch as they are where the rubber meets the road for the current supply and demand balance. While crude forward curves are telling us that there is a growing concern about crude oil supply rather than demand moving through 2021 following the vaccine announcements, it’s important to consider that the crude futures market often gets ahead of the reality on the ground or looks through short-term risk. Sometimes this speculation and willingness to look through risk pays off, sometimes not.”

Although it took months of oil demand disappointments and an accumulation of setbacks to the consensus macroeconomic global risk-on thesis to cause a sizeable correction in crude futures after a 40% rally, the selloff over the past two weeks serves as a reminder that the underlying physical market fundamentals do ultimately rein in futures prices and bring them back to reality in due time. Furthermore, the reasons behind the recent 15% selloff in oil futures should force a further evaluation of this largely consensus macro thesis. A potential turn in this consensus macro outlook that called for a weakening U.S. dollar has wide-ranging impacts across commodities and financial asset classes, and particularly for crude oil which is highly inversely correlated to the U.S. dollar.

Crude Oil and the Evolving Macro Outlook

Just a week after issuing this word of cautious optimism for oil futures, on December 11, the first Emergency Use Authorization (EUA) issued by the FDA for Pfizer-BioNTech’s COVID-19 vaccine was announced. A week after that came the EUA for the Moderna vaccine. And with these two announcements, the global macro outlook should have begun to be flipped on its head. Suddenly, there was good reason to call into question the narrative of emerging market outperformance and commensurate dollar weakness. With the U.S. set to receive vaccines for its population well before its developed Western European peers, this also pointed to relative weakness likely developing in the Eurozone economy and the Euro.

In the final week of December, the U.S. dollar index bottomed, and yields on U.S. treasury bonds surged higher – seemingly reflecting this changing macro outlook. This trend of rising U.S. treasury yields and a strengthening U.S. dollar accelerated as we moved through the first quarter. But crude oil futures shrugged off their usual inverse correlation with the dollar and these counter-expectation macro developments, surging higher as speculative bullish financial positioning continued to rise through early February.

In the first week of February, we issued this warning to DTN ProphetX® users: “With the U.S. seemingly already seeing the success of vaccines show through in COVID-19 data, and with our economic peers in the Eurozone and Asia falling behind in both procuring and administering vaccines, the U.S. economy should be expected to outperform in the near term, pulling the U.S. dollar higher. This will prove a major test for commodity markets which have experienced a broad rally amid a weakening dollar over the past year. As the dollar strengthens, the relative fundamental supply/demand tightness of each commodity market will become increasingly important.”

Silver futures peaked during the same week we issued this warning and have since traded 18% lower. Corn futures peaked one week later. Soybean futures peaked one month later. Copper peaked in late February and is now down 9% from its highs. Gold futures, which had rallied strongly throughout December, plummeted in the first week of the new year just as the U.S. dollar bottomed. The selloff in Gold intensified through Q1 as U.S. treasury yields (both real and nominal) and the dollar pushed higher. Aluminum, meanwhile, continued to surge higher moving through the end of Q1.

Crude oil futures pushed higher despite the rising U.S. dollar moving through early March. Of course, crude prices had some assistance that other commodity markets did not receive. On March 4, OPEC+ agreed to keep production limits largely unchanged and Saudi Arabia announced they would keep their additional 1 million bpd voluntary production cut in place through April. Moving into the meeting, the market consensus expectation was for a 500,000 bpd increase in output from the group.

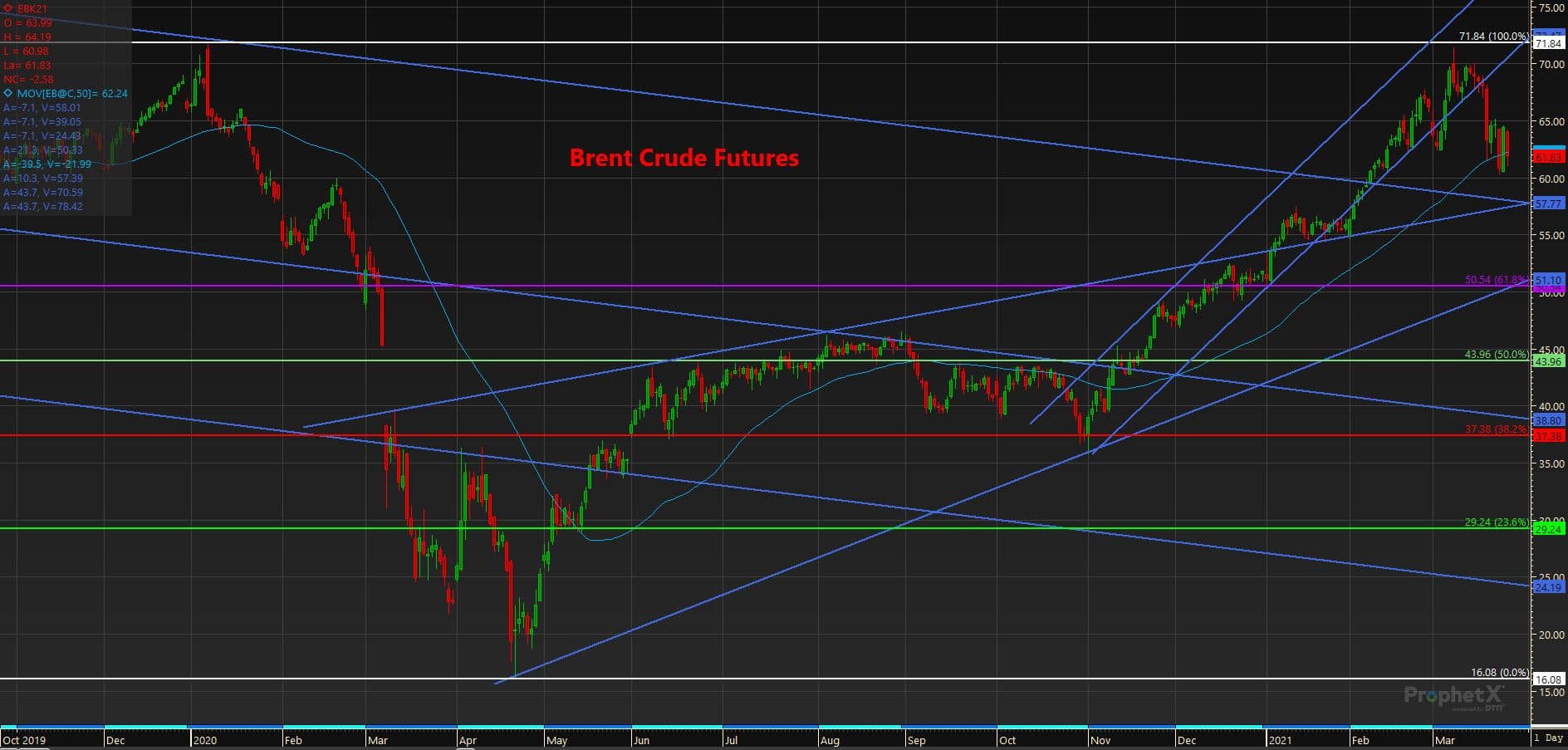

Instead of viewing this move to hold production back as a warning that Saudi Arabia was already seeing demand disappoint, crude was bid up on the news that April supply would underwhelm expectations. Days later, on March 8, a drone attack on oil storage at Saudi’s Ras Tanura facility sent prices rising to their pre-pandemic January 2020 highs, with Brent nearing $72.00 bbl.

The Brent forward curve continued to reflect extreme tightness in oil supply moving through the second week of March even though it was increasingly clear that demand developments outside of the U.S. were moving against the outlook for a normalization of global demand. India (one of the key sources of demand growth central to the 2021 bull market narrative) already had their oil minister complaining to the Saudi energy minster that high prices were hurting their economic recovery and oil demand in the lead-up to the March meeting. At the same time, according to Ursa Space Systems data, crude inventories were already once again pushing higher in China moving through February into March. And this was before peak refinery outages in China amid seasonal maintenance in the March-April period.

Priced for Perfection

Simply by looking at the trend for prompt month crude futures it should have been obvious that downside market risk was building moving into the spring. If Brent would have held on its November through early March bullish trend, this would have implied $80 prompt month crude by the first week of May and $100 by July. With India and developing nations already feeling the pain of higher oil prices in the $60s, with nearly 9 million bpd of crude production sitting on the sidelines from OPEC+, and with Europe and developing economies suffering from lack of vaccine access, $80 prompt month crude futures by May simply made no sense.

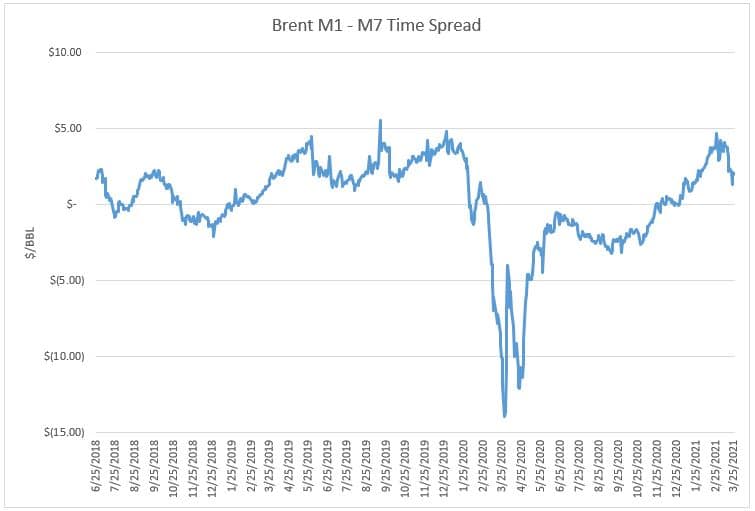

By the second week of March, the Brent six-month time spread was still trading at a $4.10 backwardation – near the 95th percentile of historical time spreads. From a market narrative perspective, justifying this sort of extreme backwardation meant expecting continued production restraint from OPEC+ members, U.S. shale production declines, no resurgence in COVID-19 in developing economies and a swift rollout of vaccine administration across the U.S. and Europe. The market was truly priced for perfection. Crude futures were set for a selloff with any significant divergence from this perfectly bullish narrative.

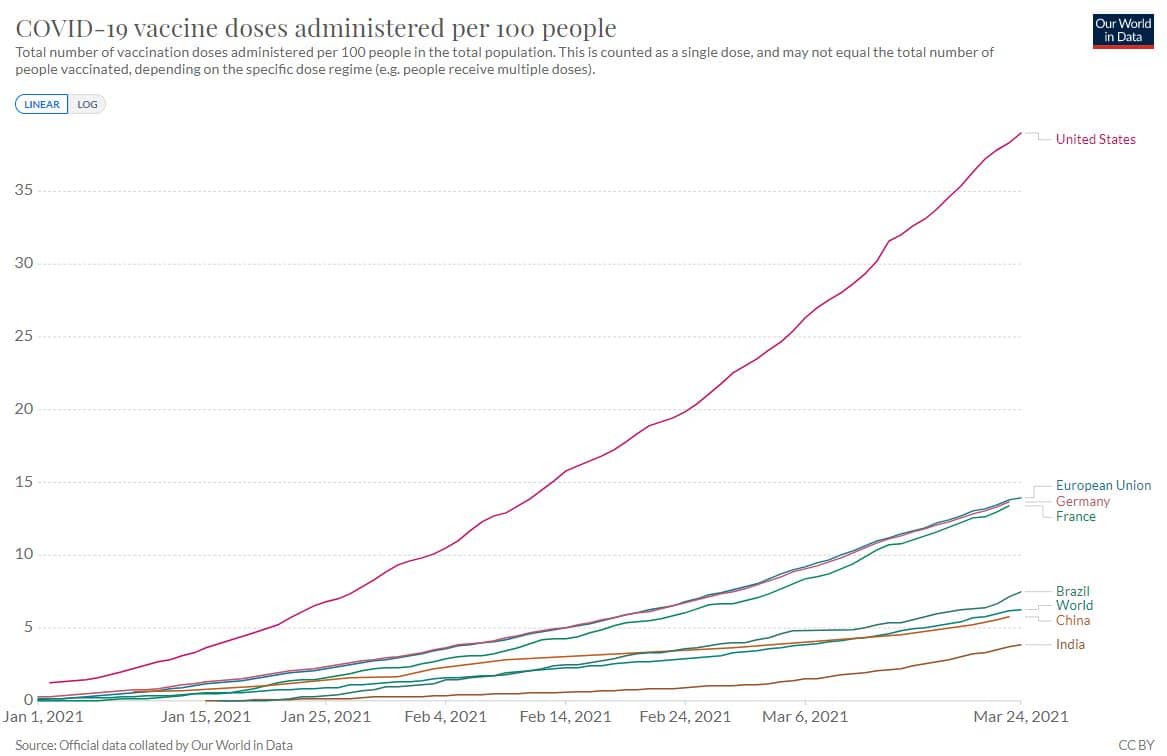

Instead of the perfect bull market storm the forecast had called for developing, demand expectations began to falter as we moved through March with COVID-19 data from outside the U.S. pointing to a resurgence of the virus. Vaccine availability and administration across the Eurozone and most emerging economies increasingly pointed to a failure to get the populations to herd immunity via vaccine anytime soon.

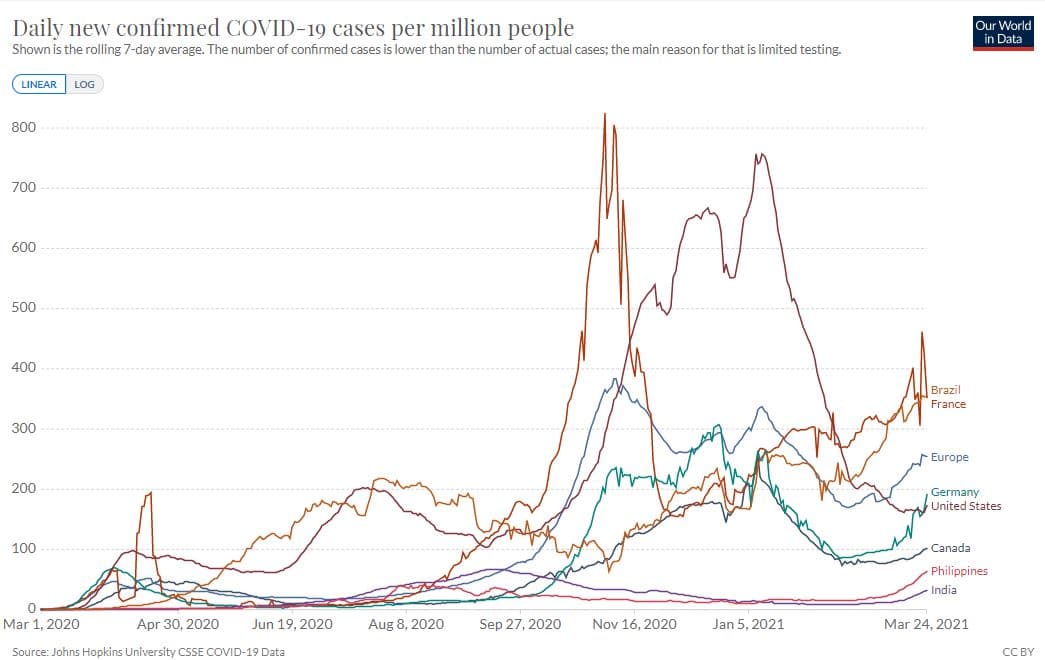

Moving into the final week of March, most regions of the globe are seeing an increase in COVID cases as variants of the virus spread. Cases are again on the rise in nearly every country in Europe except the UK, which has had the most successful vaccine program on the continent. This has prompted a renewal of government-imposed lockdown measures across Europe. Cases are surging in Southeast Asia and the Western Pacific, most notably in India and the Philippines. In South America, it is being called the worst health disaster in Brazil’s history as COVID cases and deaths rise to record highs.

U.S. Dollar Outlook

Relative U.S. macroeconomic outperformance compared to global peers, relatively strong yields on U.S. treasuries, and a trade war that pushed China toward Yuan devaluation helped drive the U.S. dollar bull market over the past decade. The U.S. dollar saw safe-haven buying interest and surged higher in the early days of the initial COVID-19 financial panic in March of 2020, but this strength was short-lived. The dollar sold off steadily throughout the rest of 2020 as the U.S. became the epicenter of the global pandemic.

As previously noted, moving into 2021, the consensus market outlook was for the U.S. dollar to continue to weaken. This view followed from a larger macro thesis that involved expectations for the Eurozone economy to outperform the U.S. and for developing economies to emerge more quickly from the economic downturn than the U.S., leading to relative opportunity in emerging economy capital markets. This weak-dollar/strong-emerging-economy and Eurozone macro trade was widely expected to continue to propel commodity prices higher through 2021 and was a consistent factor in calls for a new commodity super-cycle.

It is now clear that this macro thesis has largely been flipped on its head. Growth expectations for the U.S. economy are now not only above that of the Eurozone – a complete reversal from Q4 2020 expectations – but outlooks for the gap between U.S. and Eurozone economic growth continues to grow in America’s favor. Vaccination rates across the Eurozone and most developing economies increasingly point to a painfully slow rollout of vaccines that will weigh on economic output and oil demand through Q2.

This leads U.S. to ask the obvious question: if relative U.S. macroeconomic outperformance, relatively strong U.S. bond yields and pressure on China from the U.S. are all trends that are set to resume in 2021, what’s to stop the U.S. dollar from resuming its pre-COVID decade long bull market trend?

Yes, loose U.S. fiscal and monetary policy risks inflation. But the bond market is not pricing in some sort of sustained inflationary or extreme hyperinflationary scenario. For now, the selloff in U.S. bonds and rise in longer-term bond yields appears to be a correction or normalization of rates given the increasingly optimistic outlook for the U.S. economy.

While rising bond yields should worry the housing market and are worrying equity market investors that the Federal Reserve may raise their benchmark interest rate sooner than expected, these higher U.S. bond yields are increasingly attractive to foreign investors. Likewise, with pension and mutual funds needing to rebalance after bond prices have dropped and stocks have risen over the past quarter, this too should bring buying interest to the bond market and slow the recent rip higher in bond yields. As we work through 2021, I expect the 10-year U.S. treasury yield to continue to work toward 2%. This does not mean the multi-decade bull market in U.S. bonds is over, just that U.S. economic policy and growth will send yields to the top of their long-term downtrend before ultimately beginning to move lower once more. None of this precludes a strengthening U.S. dollar.

Conclusion

The U.S. dollar index is breaking through major technical resistance levels this week as it pushes higher heading into April and is currently working back into the bullish channel that it traded in throughout the past decade’s bull market. We see the dollar rally continuing to help inspire a short-term pullback in oil prices with the potential for another 5-10% decline from here. However, we also believe oil prices will begin moving higher alongside the dollar – bucking the typical inverse correlation – as oil demand rises through the summer.

2016 likely serves as the best possible analog for this potential scenario. By mid-2016, U.S. crude production had plummeted nearly 15% or 1.2 million bpd from its June 2015 highs following the massive bear market in crude over 2014-2015. With this weakness in U.S. production, from April-December 2016, Brent rose from $45 bbl to $56 bbl while the U.S. dollar index rallied from 93 to 103 over the period.

Similarly, in today’s market, U.S. crude production is down 2 million bpd or just over 15% from its pre-pandemic highs. And with U.S. producers doubling down on their commitment to production restraint during this bull market, the lack of supply will force the U.S. to become an increasingly larger net import of crude this year. If OPEC+ producers can also maintain restraint while global demand recovers, this could certainly allow for crude prices to continue modestly higher this summer despite U.S. dollar strength. Longer term, however, it is unlikely that oil prices will be able to avoid being pulled lower by the weight of a rising dollar.

You can be bullish crude because you believe the hyper-growth phase for U.S. shale will never return. You can be bullish on expectations of demand growth over the coming decade. You can be bullish because you believe underinvestment in production in recent years will lead to a shortfall of supply and an exhaustion of OPEC spare capacity. But timing and scale matter. These may be reasons to invest in the oil sector and to buy equity shares in oil producers, but these reasons did not and do not justify $80 or $100 crude prices this spring or summer. We believe a $60-72 trading range for Brent is far more realistic and a strengthening dollar will help reinforce this outlook.