Comprehensive weather insights help safeguard your operations and drive confident decisions to make everyday mining operations as safe and efficient as possible.

Comprehensive weather insights help safeguard your operations and drive confident decisions to make everyday mining operations as safe and efficient as possible. Learn how to optimize operations with credible weather and environmental intelligence. From aviation safety to environmental compliance, our comprehensive suite of solutions delivers real-time insights, advanced forecasting, and precise monitoring capabilities.

Learn how to optimize operations with credible weather and environmental intelligence. From aviation safety to environmental compliance, our comprehensive suite of solutions delivers real-time insights, advanced forecasting, and precise monitoring capabilities. Headwinds for Oil Grow as Economic Recovery Falters

Key Developments:

- Distillate fuel oil stocks continue to rise despite surging net exports and weakness in refinery runs.

- Adjustment factor analysis points to U.S. crude production rising nearly 1.0 million bpd since early June.

- We believe further weakness in the U.S. dollar can lead WTI higher from here, but that WTI is likely to find a confluence of fundamental and technical resistance as it nears the $44.00 bbl level.

Crude prices have pushed higher this week despite Wednesday’s bearish fundamental data release by the EIA. So far this week, the plummeting U.S. dollar has overshadowed fundamental data which point to rising U.S. crude production and renewed weakness in demand amid the weight of the growing COVID-19 pandemic. Even with surging refined product exports and weakness in refinery runs, product stocks are continuing to build. With peak seasonal gasoline demand just around the corner, the outlook for refinery runs looks bleak. We believe further weakness in the U.S. dollar can lead WTI higher from here, but upside is limited given persistent weakness in underlying fundamentals.

Crude Production and the Adjustment Factor

This time last month, we estimated that U.S. crude production was already on the rise by 400,000-500,000 bpd. We called for the EIA’s adjustment factor to soon flip from negative to positive territory. As we stated at the time, “For further confirmation that U.S. crude production is back on the rise, we should watch for the adjustment factor flipping into positive territory in the coming weeks. Just as the EIA underestimated the rate of production cuts in recent months, a quick turnaround in U.S. production is also likely to be underestimated in the production estimate and lead to a positive adjustment factor.”

Large gaps between EIA and real-time ship tracking data for crude net imports in recent weeks have allowed for explainable volatility in the adjustment factor that continued to point to a recovery in domestic crude production. EIA data for the week ending July 17 provided further confirmation of this outlook.

This week, the adjustment factor accounted for the largest share of week-on-week change for any variable in the crude balance. As we had forecast, the adjustment factor moved into positive territory, rising 1.6 million bpd week-on-week to average 857,000 bpd in the week ending July 17. At 857,000 bpd, this was the first positive adjustment factor recorded in weekly EIA data since the week ending April 24 and the largest positive adjustment factor since the week ending April 10.

We do not believe the entirety of this 857,000 bpd is attributable to a rise in domestic production. Vessel tracking data point to the EIA underestimating net imports of crude by a significant margin during the week, which also necessitated the positive adjustment factor. Given the size of the adjustment factor, and that the EIA raised their official production estimate by 100,000 bpd to 11.1 million bpd on the week, we believe that actual domestic crude production is already closer to 11.4 million bpd.

Refinery Runs

The EIA reported refinery runs ticking slightly lower last week, ending an eight-week consecutive run of rising crude oil inputs at U.S. refiners. As summer driving season draws to a close, we are now just 3 weeks away from the historical seasonal peak in refinery runs.

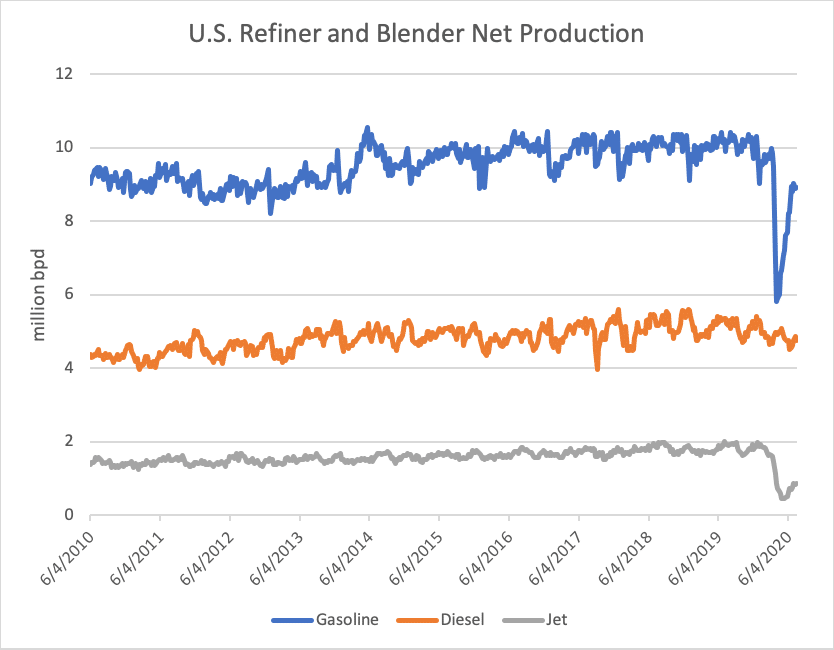

EIA data show that U.S. refiners have been prioritizing production of gasoline over diesel and jet fuel as one might expect given the relatively swift recovery in gasoline demand this summer. Refiner and blender net production of gasoline has increased 3.1 million bpd from the low set in the week ending April 3, while distillate fuel oil and jet fuel production is still down 220,000 bpd and 6,000 bpd, respectively from the same period. In the week ending July 17, refiner and blender net production of distillate fuel oil was its lowest for the seasonal period since July 2012.

At 14.3 million bpd, net inputs of crude at U.S. refiners are down 17%, or 2.8 million bpd, from year-ago levels. The rate at which refinery runs are growing relative to year-ago levels is slowing both on a week-on-week and three-week moving average basis. Compared to year-ago levels, refinery runs were rising at a peak rate of 3.6% in late May. This has now slowed to just 0.6% in the week ending July 17. Without an unexpected swift recovery in jet fuel and diesel demand over the coming month, refinery runs appear destined to turn lower before ever getting to within 90% of the prior five-year average or year-ago levels.

Refined Product Demand and Distillate Stocks

High frequency data from DTN show gasoline and diesel demand peaking around the 4th of July holiday and then falling to a lower plateau so far this month. This aligns with the EIA’s own demand proxy, product supplied, which shows demand for distillate fuel oil and gasoline turning lower from their late June/early July peak. The four-week moving average for total product supplied declined for the first time since the final week of May in this week’s EIA data release, emphasizing a broader trend of declining product demand following the holiday.

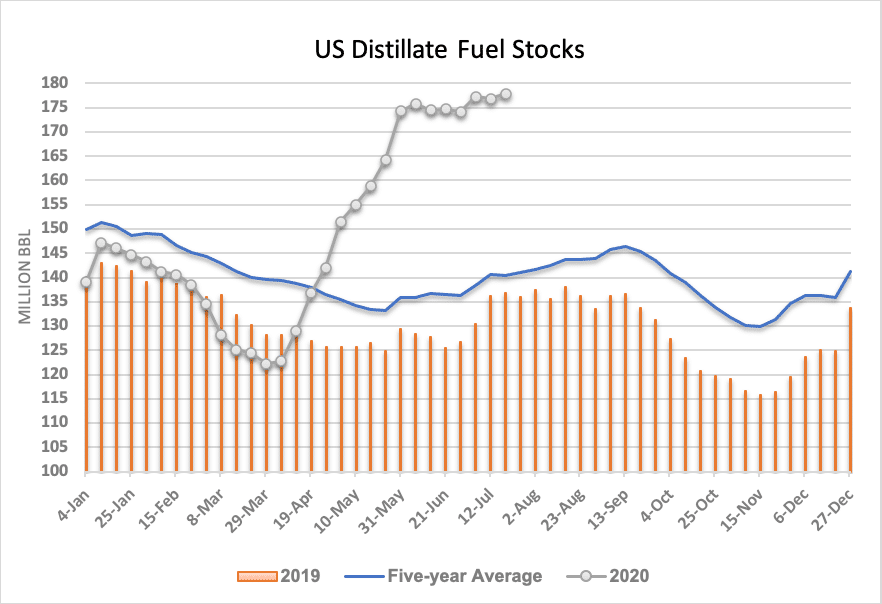

This week’s EIA data revealed distillate fuel oil stocks rising 1.1 million bbl from the prior week to 177.9 million bbl – just shy of the record-high set in December of 1982. Builds in distillate fuel oil stocks come despite the EIA reporting surging net exports of the fuel, and refinery runs averaging 17% below year-ago levels. Exports of distillate fuel oil were reported 48%, or 467,000 bpd, above year-ago levels for the week, while imports were down 50%, or 53,000 bpd, year-on-year.

Further builds to distillate fuel oil stocks despite surging net exports of the fuel, and continued weakness in refinery runs reflects the sharp economic contraction weighing on domestic diesel demand as well as U.S. refiners blending the jet fuel pool into the diesel stream amid the pronounced downturn in air travel and jet fuel refining margins.

Conclusion

Domestic crude production is pushing higher just as refined product demand and refinery runs are plateauing. This continues to emphasize the importance of the global market’s ability to absorb excess U.S. crude and refined products as we have discussed in recent weeks. We believe further weakness in the U.S. dollar can lead WTI higher from here, but that WTI is likely to find a confluence of fundamental and technical resistance as it nears the $44.00 bbl level.